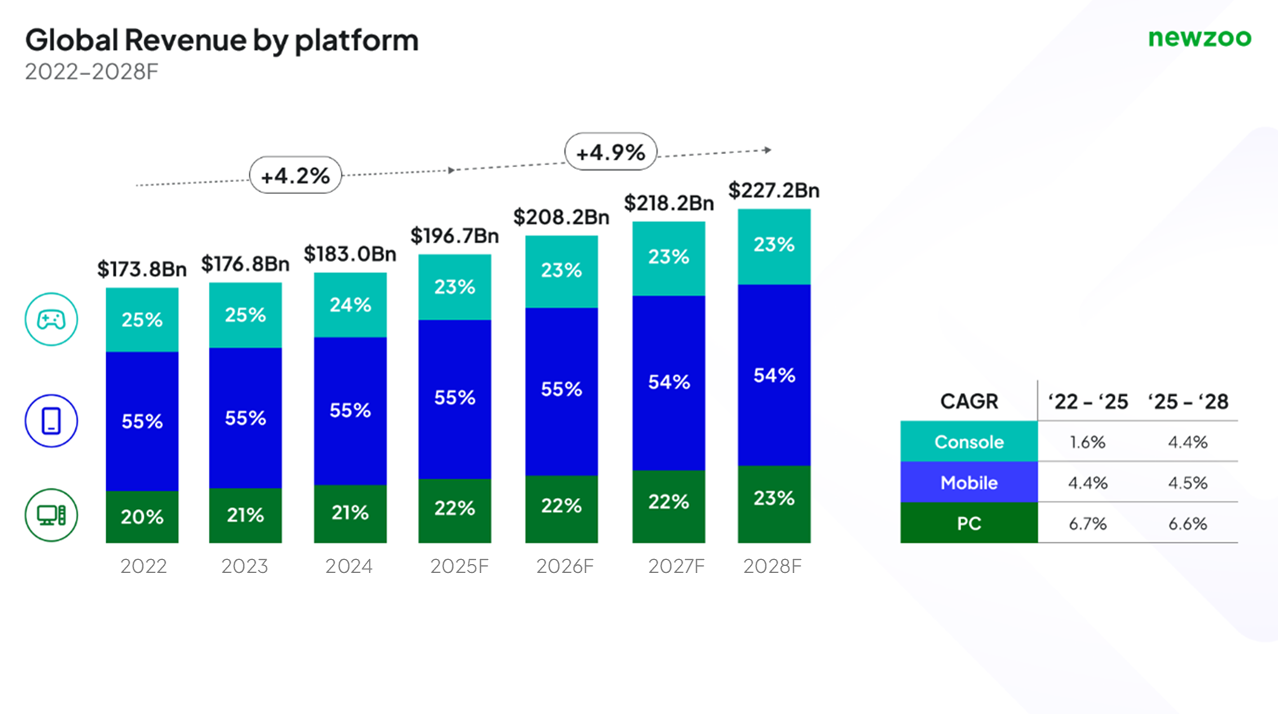

The global game market is projected to reach US$ 17 billion in 2025, driven by deep user participation

According to Newzoo’s Global Game Market Report and Forecast 2025, this year has been a remarkable one for the game industry. The launch of a large number of quality buy-out games, the sale of Switch 2 in Nintendo and the continued momentum of mobile games have collectively contributed to higher-than-expected market growth. Despite pressure from the development and distribution end, such as the reorganisation and closure of the studio, the consumption side has shown strong resilience. The level of participation and consumption of players in heavy, out-of-pocket, new and service-type games remained stable, providing a solid basis for industry. The global game market is over-anticipated: projected at US$ 17 billionThe global game market is expected to reach $70 billion in 2025, an increase of 7.5 per cent over the same period. This projection is due mainly to the strong performance of the PC and the mobile platform: The estimated income from mobile games is $108 billion (7.7 per cent over the same period)., supported by the new fire engine and the industry’s game of youth. The Chinese nuclear game continues to attract the attention and consumption of players, as demonstrated by the publishers of the century of China and China. For the second year in a row, the plate grew, indicating that after the outbreak it had returned to a steady development trajectory. The projected revenue from mainframe games is $45 billion (4.2 per cent over the same period)The growth has been driven by the Switch 2 distribution in Nintendo and the intense launch of the classic IP. PC game projected revenue of $43 billion (10.4 per cent over the same period)A set of quality buy-out games outperformed last year ‘ s star product, confirming that high-quality content can still break out of the PC market with increased competition.

Newzoo’s chief market analyst, Michel Buijsman, stated: “The growth in 2025 was not due to a proliferation of players’ base numbers, but rather to deeper consumption by players in the game and ecology they had recognized.” New performance in 2025: double-dimensional perspective of revenue and participationIn its report, Newzoo tracks the new income performance of the PC in January-November 2025 in six countries in Europe and the United States (United States, United Kingdom, France, Germany, Italy, Spain).

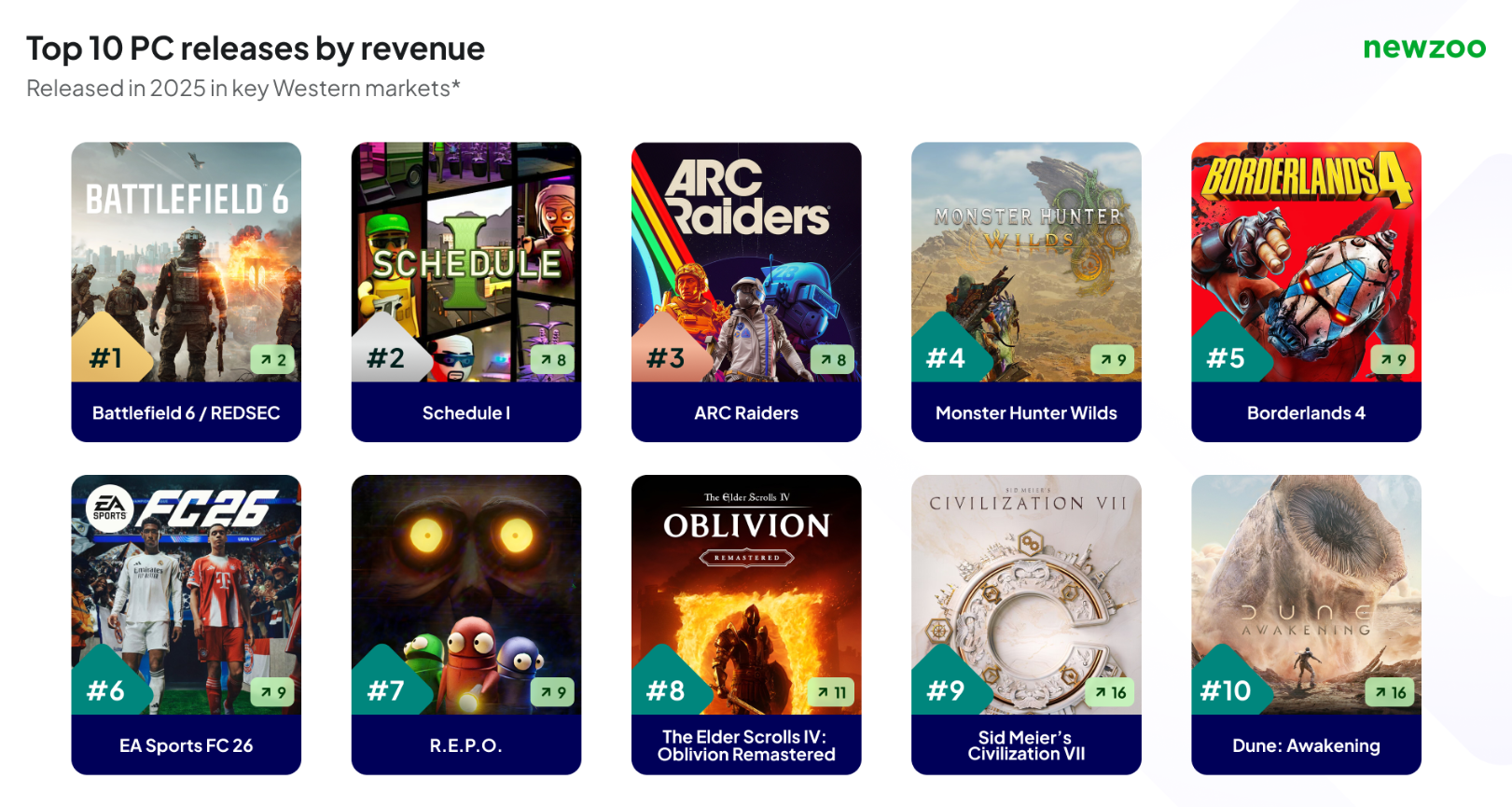

PC Market:The fact that buy-out games drive the growth of PC revenues, with the top 10 being out-of-manufacturing products, highlights the dependence of the PC market this year on full-paying games. PC continues to provide space for medium-sized studios and new IPs, with ARC Raiders, Scheduule I, R.E.P.O., and Sand dunes: Awakening, among others, at the top 10, reflecting the relative openness of the PC platform to new IP and system-driven design. The diversity of types remains a distinct advantage for the PC, with the top 10 games covering six different categories. The shooting game continues to be the largest category of the PC and its successful paths are diversified (covering tactical, cooperative, saping, etc.). Host market (mainly new to PlayStation, Xbox and Switch platforms)

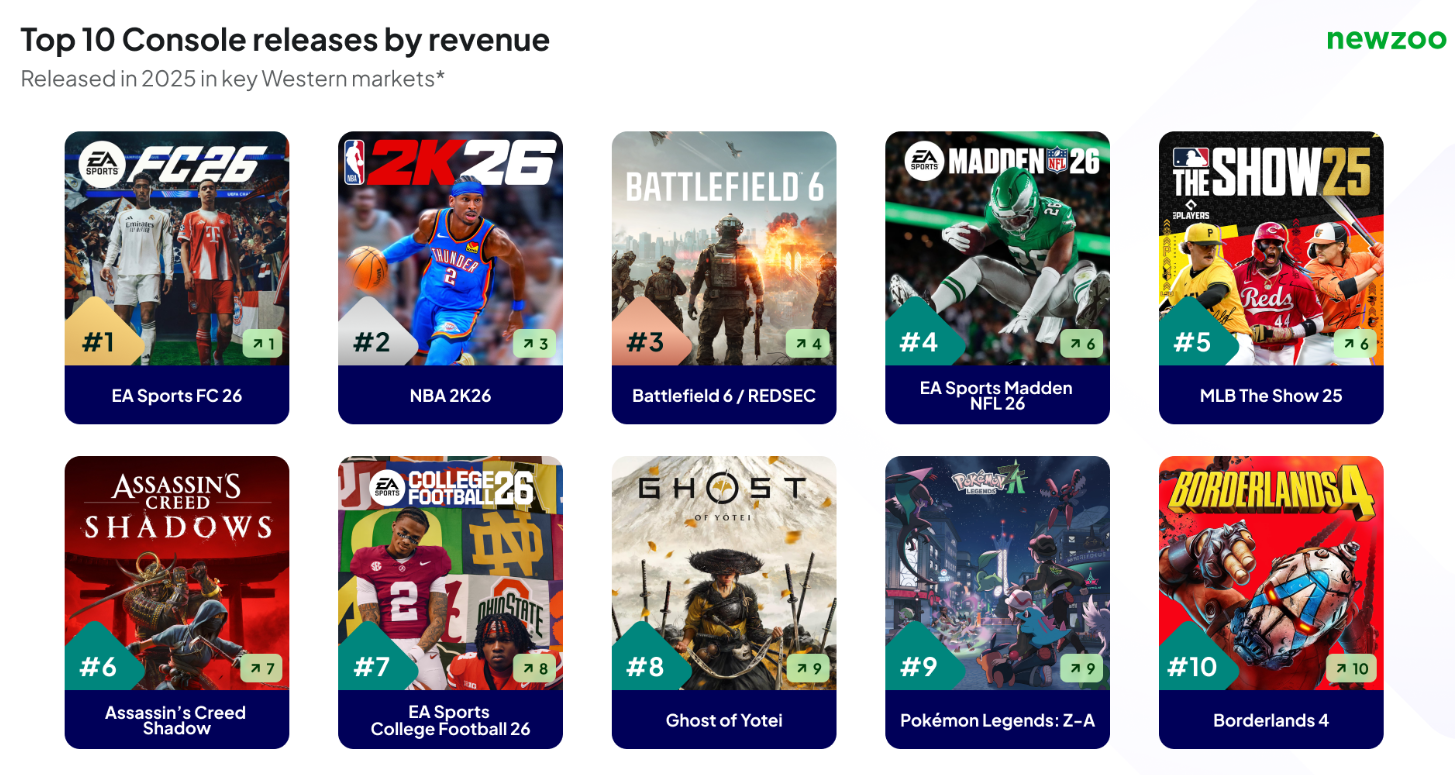

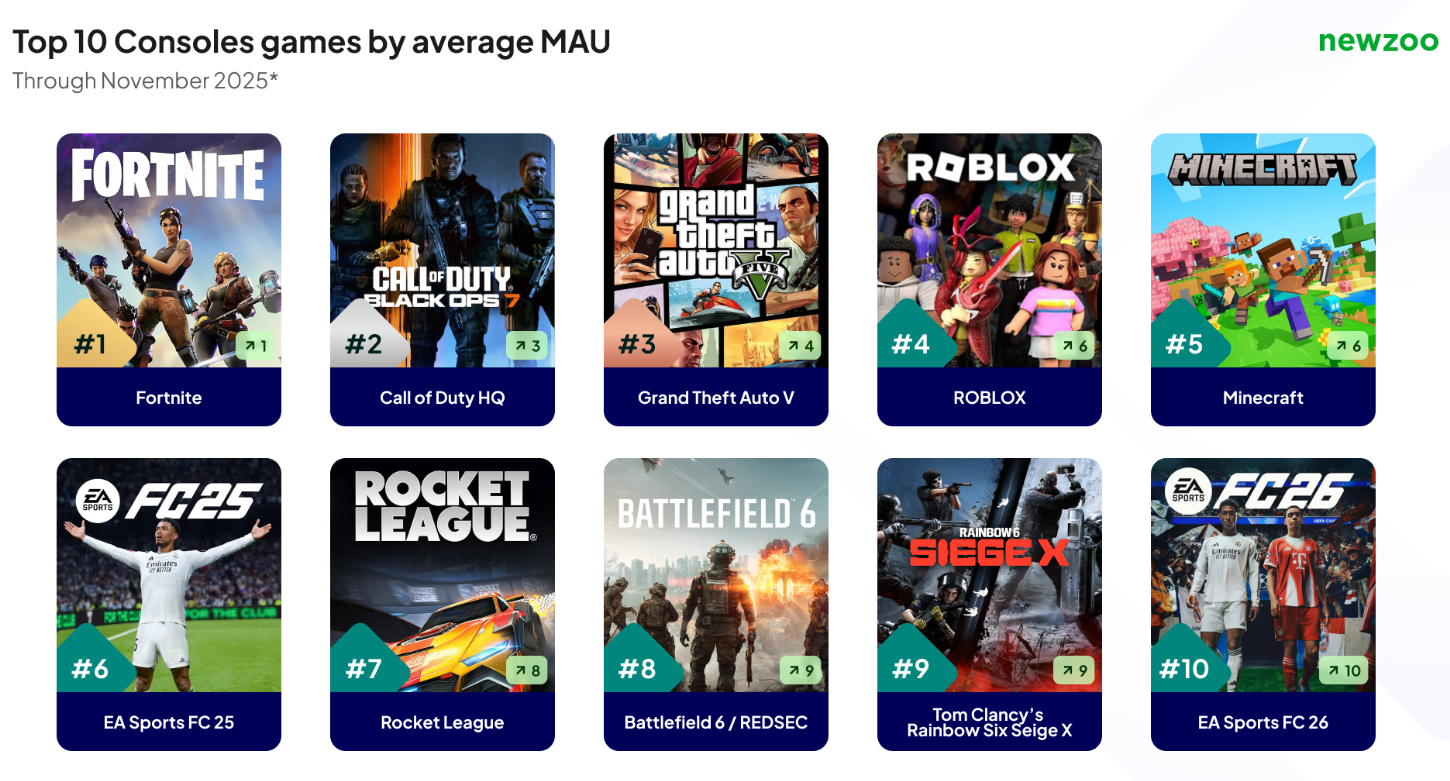

Level 3A IPs dominate the top 10 hosts, with large distributors and mature IPs accounting for most of the revenues. With four games leading the list, the EEA sports game combination and strong buyout distribution strategy have been very effective. Sports games occupy the top 10 half of the mountain and are an annual series, which attests to the persistence of the customary game and stable distribution cycles of the host platform. The platform remains influential: the dream legend Z-A, though landing only on a single platform, ranks ninth on the income list, of which about half comes from Switch 2. Taken together, the PC and host income list clearly demonstrates the division of value creation paths: the PC favours diversity, deep content and new IPs, while the host income remains anchored to the size effect, series IPs and custom games. Player ParticipationService-type games dominate the monthly active list of PC and host users, such as Fort Night, My World, Roblox and others, with continuous renewal, social systems and creators’ ecology. Only one of the new ones in 2025, with a significantly broader user base with a free expansion, succeeded in reaching the top 10 monthly Platform activities. The shooting game prefers to divide the platform: the PC shooting game places greater emphasis on sophistication and accuracy, while the host shooting game focuses more on hand-in-hand and IP familiarity. The participation of the annual cargo series at the host end was better than that of the PC, reflecting differences in the user participation patterns of different platforms. Overall, participation data reinforce a cross-cutting theme in 2025: continuous playtime and content updates that attract longer-term attention than mere distribution times.

Related Posts

TikTok was reported by the Indonesian Electronic Logistics Association to the inspection agency. Break

Iron Fist 8 was bombed by a bad player because of the third season update and the official commitment to repair it urgently.